This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

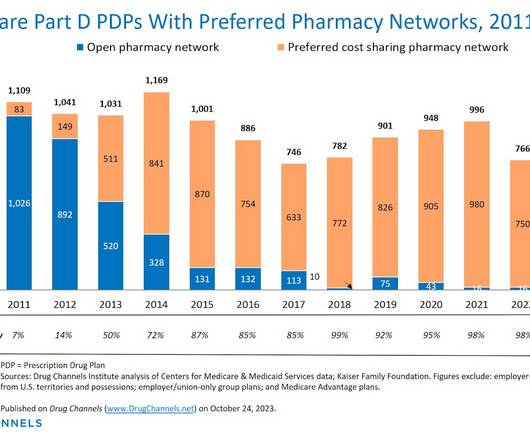

In a previous article , I highlighted the largest pharmacy chains that will participate in the 2024 Medicare Part D prescription drug plans (PDP). Plans from Aetna, Humana, WellCare, and UnitedHealthcare will not have any independentpharmacies participating via PSAOs as preferred pharmacies. Look out below!

Our exclusive analysis of Center for Medicare & Medicaid Services’ (CMS) data reveals that preferred cost sharing pharmacy networks will maintain their dominance as a component of Part D benefit design. In upcoming articles, I’ll delve into chain and independentpharmacies’ participation in the major 2024 preferred networks.

In this issue: Payers confess: Patients lose from copay accumulators Humana joins the Express Scripts GPO Hospitals vs. PBMs over specialty pharmacy white bagging Let’s all follow the Buy-and-Bill Dollar! Plus, entrepreneurial pharmacy owner Dave Marley demonstrates the power of innovation. Sometimes, the little guy wins big.

Among these, pharmacy benefit managers (PBMs) play a crucial role, handling reimbursements and negotiations with drug manufacturers and pharmacies. Three major PBM players – CVS Caremark, Express Scripts, and OptumRx – collectively command a significant 79% market share , orchestrating much of the industry’s dynamics.

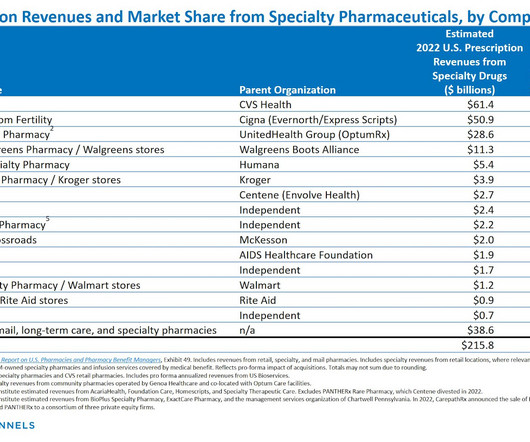

Last week, we examined the growing concentration of specialty drug dispensing revenues among the largest pharmacies. See The Top 15 Specialty Pharmacies of 2024: How PBMs, Health Systems, and Independents Are Shaping the Market. Today, we dive deeper. Drawing from DCIs new 2025 Economic Report on U.S.

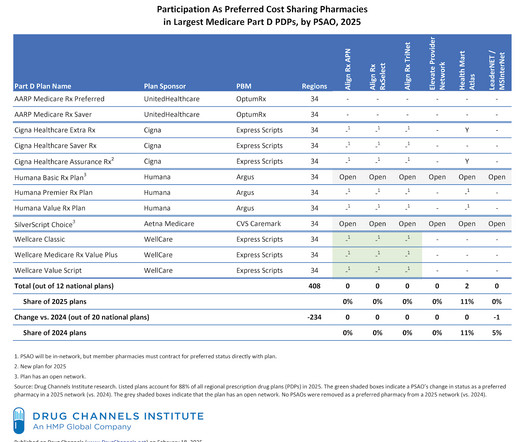

Small pharmacies have ghosted Medicare Part Ds preferred networksno farewell party, no breakup text, just a quiet exit. A few months ago , DCI highlighted how the largest pharmacy chains are participating as preferred cost sharing pharmacies in the 2025 stand-alone prescription drug plan (PDP) networks. Abracadabra!

We organize all of the trending information in your field so you don't have to. Join 15,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content